15 Real Estate Terms Every Buyer Should Know: Navigating the complex world of real estate can feel overwhelming, especially for first-time buyers. Understanding key terminology is crucial to making informed decisions and avoiding costly mistakes. This guide breaks down 15 essential real estate terms, empowering you to confidently navigate the home-buying process and secure your dream property. From understanding the difference between listing price and appraisal value to grasping the intricacies of earnest money deposits and mortgage pre-approval, we’ll equip you with the knowledge you need to succeed.

This isn’t just a glossary; it’s a strategic roadmap designed to demystify the jargon and empower you to negotiate effectively. We’ll explore critical concepts like contingencies, closing costs, and the roles of real estate agents and brokers, providing practical examples and insights to help you make smart financial choices. By the end, you’ll possess a solid foundation of real estate knowledge, allowing you to approach the home-buying journey with confidence and clarity.

Introduction

Buying your first home is a significant milestone, and understanding the basics of real estate is crucial for a smooth and successful process. Real estate, simply put, refers to land and any permanent structures attached to it. This includes everything from the ground itself to the buildings, improvements, and even the natural resources located on it. Navigating the world of real estate can seem daunting, but with a little knowledge, the process becomes much more manageable.Real estate encompasses a wide variety of property types, each with its own set of characteristics and investment considerations.

The most common categories include residential, commercial, industrial, and land. Residential real estate involves properties designed for living, such as single-family homes, apartments, condos, and townhouses. Commercial real estate focuses on properties used for business purposes, including office buildings, retail spaces, and shopping malls. Industrial properties are those used for manufacturing, warehousing, or distribution, while land encompasses undeveloped tracts of property suitable for various uses.

Types of Real Estate Properties

Residential real estate is the most familiar type for most buyers. Examples include detached houses, semi-detached houses, townhouses, condominiums, and apartments. These properties are primarily used for living purposes and are often purchased for personal use or as rental investments. Commercial real estate, on the other hand, encompasses properties used for business activities. This includes office buildings, retail stores, shopping centers, and hotels.

These properties are typically purchased as investments, aiming to generate rental income or appreciate in value. Industrial properties such as factories, warehouses, and distribution centers cater to manufacturing, storage, and logistics operations. Finally, land itself can be a significant real estate asset, purchased for development, investment, or agricultural purposes.

Common Real Estate Transactions

Several common transactions occur within the real estate market. The most prevalent is the sale and purchase of a property, where a buyer agrees to purchase a property from a seller at an agreed-upon price. Another common transaction is refinancing, where a homeowner replaces their existing mortgage with a new one, often to secure a lower interest rate or access more equity.

Rental transactions involve the leasing of property to tenants, with the owner receiving regular rental payments in exchange for the use of the property. Finally, property development involves the construction or renovation of properties for sale or lease, often representing a more complex and potentially higher-risk investment. For example, a developer might purchase a vacant lot, obtain necessary permits, and construct a residential building to sell individual units.

Listing Price vs. Asking Price vs. Appraisal Value

Understanding the difference between listing price, asking price, and appraisal value is crucial for navigating the real estate market successfully. These three figures represent different aspects of a property’s worth, and their interplay can significantly impact a buyer’s negotiation strategy and overall experience. While they are often used interchangeably in casual conversation, they hold distinct meanings and implications.

The listing price, asking price, and appraisal value each reflect a different perspective on a property’s worth. The listing price is the initial price set by the seller’s agent, often based on comparable properties and market analysis. The asking price is the price the seller is willing to accept for the property; it can be the same as, higher than, or lower than the listing price.

Finally, the appraisal value is an independent professional estimate of the property’s market value, conducted by a licensed appraiser. This valuation is often crucial for securing a mortgage.

Factors Influencing Listing Price

Several factors influence a seller’s listing price. These include the property’s location, size, condition, features (like a swimming pool or updated kitchen), comparable sales in the neighborhood (comparative market analysis or CMA), and current market trends (supply and demand). A seller’s agent uses this information to establish a competitive yet realistic starting point for negotiations. For example, a larger home in a desirable school district will likely have a higher listing price than a smaller home in a less desirable area, even if both are in similar condition.

Factors Influencing Asking Price

The asking price is determined by the seller, often in consultation with their real estate agent. It considers the listing price, market feedback (offers received, competing properties), the seller’s motivation (e.g., urgent need to sell), and any emotional attachment to the property. A seller might initially ask for a higher price, hoping to receive a better offer, or they might be more flexible if they are facing time constraints.

The asking price is a dynamic figure that can be adjusted throughout the sales process.

Factors Influencing Appraisal Value

The appraisal value is an objective assessment of a property’s worth based on a licensed appraiser’s analysis. They consider factors such as the property’s location, size, condition, features, comparable sales (recent sales of similar properties), market conditions, and any economic factors impacting the local real estate market. The appraiser uses various methodologies, including the sales comparison approach, the cost approach, and the income approach, to arrive at a fair market value.

An appraisal is often required by lenders to ensure the property’s value justifies the loan amount.

Comparison of Listing Price, Asking Price, and Appraisal Value

| Price Point | Description | Influencing Factors | Impact on Buyer |

|---|---|---|---|

| Listing Price | Initial price set by the seller’s agent. | Comparable sales, market trends, property features, location. | Provides a starting point for negotiations; may be higher or lower than the final sale price. |

| Asking Price | Price the seller is willing to accept. | Listing price, market feedback, seller’s motivation, comparable properties. | Negotiation target; can influence offer price; may differ from appraisal value and final sale price. |

| Appraisal Value | Independent professional estimate of market value. | Comparable sales, property condition, location, market conditions, appraiser’s methodology. | Crucial for securing a mortgage; may influence the final sale price or necessitate renegotiation. |

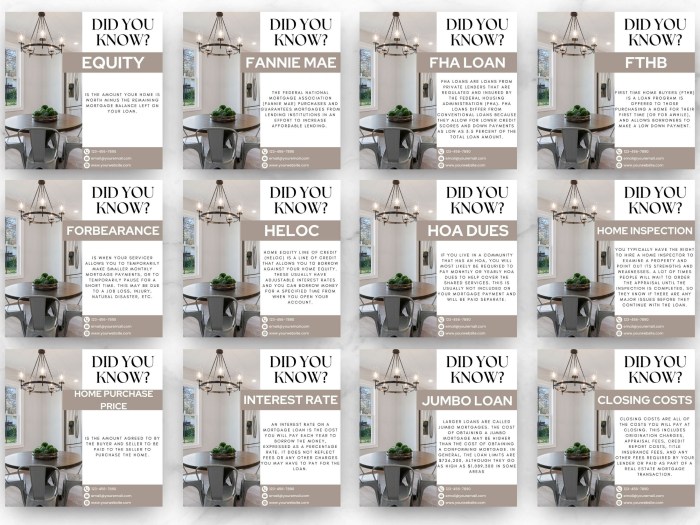

Earnest Money Deposit

An earnest money deposit is a crucial part of the home-buying process, demonstrating your commitment to purchasing the property. It’s a good-faith payment that shows the seller you’re serious about the offer and reduces their risk of the deal falling through. This deposit is held in escrow by a neutral third party, typically a title company or real estate attorney, until the closing of the sale.The earnest money deposit serves several important functions.

It assures the seller that you, the buyer, are financially capable and genuinely interested in buying their house. It also provides a degree of protection for the seller should you back out of the contract without a valid reason as defined in the purchase agreement. This protection is not absolute, and the exact circumstances that allow the seller to retain the earnest money will vary depending on state laws and the terms Artikeld in the purchase agreement.

Earnest Money Deposit Percentage Range

The typical range for an earnest money deposit is between 1% and 5% of the purchase price. However, this percentage can be negotiated between the buyer and seller and is often influenced by market conditions and the specifics of the property. In a highly competitive seller’s market, a higher earnest money deposit might strengthen your offer, showing the seller you’re a serious and committed buyer.

Conversely, in a buyer’s market, a lower percentage might be acceptable. The deposit amount is usually stated clearly within the purchase agreement.

Consequences of Failing to Provide the Earnest Money Deposit

Failure to provide the earnest money deposit as stipulated in the purchase agreement can have significant consequences. The seller might consider your offer invalid and move on to another buyer. Depending on the terms of the contract, the seller may also be entitled to pursue legal action to recover any damages they may incur as a result of your breach of contract.

This could include costs associated with finding a new buyer or any losses experienced due to the delay in selling the property. The specific repercussions will vary greatly based on local laws and the specific terms of the purchase agreement. Therefore, it’s essential to understand and fulfill all obligations Artikeld in the contract.

Mortgage Loan Basics (Principal, Interest, Taxes, Insurance – PITI): 15 Real Estate Terms Every Buyer Should Know

Understanding your mortgage payment is crucial for responsible homeownership. The acronym PITI – Principal, Interest, Taxes, and Insurance – represents the four main components of your monthly mortgage payment. Knowing how each part contributes to your overall cost helps you budget effectively and avoid financial surprises.Understanding the breakdown of your monthly mortgage payment is essential for effective financial planning.

Each component plays a significant role in determining your total cost of homeownership.

PITI Components

Your monthly mortgage payment is comprised of four key elements: Principal, Interest, Taxes, and Insurance. Principal is the actual loan amount you borrowed to purchase the home. Interest is the cost of borrowing that money, calculated as a percentage of the outstanding principal balance. Property taxes are levied by local governments to fund public services, and homeowners insurance protects your property from damage or loss.

Principal

The principal portion of your mortgage payment goes directly towards reducing the outstanding loan balance. In the early stages of a mortgage, a larger portion of your payment goes towards interest, while the principal repayment increases over time. For example, on a 30-year, $300,000 mortgage, the initial payments may allocate a smaller amount to principal, say $200, gradually increasing to a larger amount, perhaps $1,000, as the loan progresses.

This shift reflects the amortization schedule of the loan.

Interest

Interest is the cost you pay for borrowing money. It’s calculated based on your loan’s interest rate and the outstanding principal balance. A higher interest rate means a larger interest portion in your monthly payment. For instance, a 5% interest rate on a $300,000 mortgage will result in a higher monthly interest payment compared to a 3% interest rate on the same loan amount.

Taxes

Property taxes are typically paid annually but are often included in your monthly mortgage payment through an escrow account managed by your lender. The amount varies depending on the property’s assessed value and local tax rates. These funds are held by the lender and paid to the relevant tax authority on your behalf. For example, a property assessed at $300,000 in a jurisdiction with a 1% property tax rate would result in an annual tax payment of $3,000, or $250 per month.

Insurance

Homeowners insurance premiums are also typically included in your monthly mortgage payment via escrow. This insurance protects your property against various risks, such as fire, theft, and liability. The premium amount depends on factors like the property’s location, value, and coverage level. A home in a high-risk area, for instance, will typically command a higher insurance premium than a similar home in a low-risk area.

The monthly insurance cost could range from $50 to several hundred dollars depending on these factors.

Impact of Interest Rates on Monthly Payments

The interest rate significantly impacts your monthly mortgage payment. A higher interest rate leads to a substantially higher monthly payment. Consider a $300,000, 30-year mortgage:

| Interest Rate | Approximate Monthly Payment (excluding taxes and insurance) |

|---|---|

| 3% | $1,265 |

| 4% | $1,432 |

| 5% | $1,610 |

As this table illustrates, even a small increase in the interest rate can result in a noticeable increase in your monthly payment over the life of the loan. This highlights the importance of securing a favorable interest rate when obtaining a mortgage.

Pre-Approval vs. Pre-Qualification

Understanding the difference between pre-approval and pre-qualification for a mortgage is crucial for homebuyers. Both processes give you an idea of how much you can borrow, but they differ significantly in their depth and impact on your home-buying journey. Choosing the right path will significantly influence your negotiating power and overall experience.Pre-approval and pre-qualification are both preliminary steps in the mortgage process, designed to give homebuyers an estimate of how much they can borrow.

However, they differ greatly in the level of scrutiny and the resulting certainty. Pre-qualification involves a less rigorous review of your financial information, while pre-approval involves a more thorough examination, including a credit check and verification of your income and assets.

Pre-Qualification Process and Requirements

Pre-qualification typically involves a brief conversation with a lender, providing basic financial information such as your income, debts, and desired down payment. The lender will then provide a rough estimate of how much you might be able to borrow. This process is relatively quick and easy, often taking only a few minutes. However, it doesn’t guarantee you’ll receive a loan.

The requirements are minimal; you’ll need to provide general estimates of your financial situation. This process is helpful for getting a general idea of your borrowing power before starting your home search, but it shouldn’t be considered a firm commitment from the lender.

Pre-Approval Process and Requirements, 15 Real Estate Terms Every Buyer Should Know

Pre-approval, on the other hand, is a much more comprehensive process. The lender will conduct a thorough review of your credit report, verify your income and employment history, and assess your debt-to-income ratio (DTI). This process takes longer, typically a few days to a week, but it provides a much stronger indication of your borrowing capacity. Requirements include providing detailed financial documentation, such as pay stubs, tax returns, and bank statements.

The lender will also pull your credit report, which might slightly impact your credit score. A pre-approval letter is a powerful tool when making an offer on a home, demonstrating to sellers that you are a serious and qualified buyer.

Benefits and Drawbacks of Pre-Qualification

Pre-qualification offers a quick and easy way to gauge your borrowing power, allowing you to begin your home search with a general understanding of your budget. However, it lacks the certainty of pre-approval, meaning the final loan amount could differ significantly from the initial estimate. This can lead to disappointment or the need to adjust your home search strategy.

It also offers minimal negotiating leverage when making an offer on a home.

Benefits and Drawbacks of Pre-Approval

Pre-approval offers a significant advantage in the home-buying process. The detailed review of your finances provides a much more accurate picture of your borrowing capacity. The pre-approval letter serves as strong evidence to sellers that you are a serious and qualified buyer, significantly improving your chances of having your offer accepted, especially in competitive markets. However, the process is more time-consuming and requires more detailed documentation.

Furthermore, the hard credit pull associated with pre-approval can slightly lower your credit score, though this is usually temporary and the benefit of a strong offer often outweighs this minor impact.

Contingencies in a Real Estate Contract

Contingencies are crucial components of a real estate purchase agreement. They act as safety nets for both buyers and sellers, protecting each party from unforeseen circumstances that could jeopardize the deal. Understanding these contingencies is essential for a smooth and successful transaction. They essentially allow either party to back out of the contract under specific, pre-defined conditions.A contingency is a condition that must be met before the contract is legally binding.

If the condition isn’t met, the contract can be terminated, usually with the return of any earnest money deposit. The inclusion and specifics of contingencies are negotiated between the buyer and seller and are vital for managing risk throughout the purchasing process. Failing to understand these clauses can lead to significant financial and legal ramifications.

Financing Contingency

A financing contingency protects the buyer if they are unable to secure a mortgage loan. This clause specifies that the buyer’s obligation to purchase the property is contingent upon obtaining financing under agreed-upon terms, such as a specific interest rate or loan amount. If the buyer fails to obtain financing within the stipulated timeframe and under the specified conditions, they can legally withdraw from the contract without penalty.

The seller, however, is not obligated to wait indefinitely for the buyer to secure financing. The timeframe for securing financing is usually clearly defined within the contingency clause. For example, the buyer might have 30 days to obtain loan approval.

Appraisal Contingency

The appraisal contingency protects the buyer from overpaying for the property. It stipulates that the buyer is only obligated to purchase the property if an independent appraisal values the property at or above the agreed-upon purchase price. If the appraisal comes in lower, the buyer may be able to renegotiate the price, walk away from the deal, or seek additional financing to cover the difference.

This contingency is particularly important in competitive markets where properties might be listed above their true market value. For instance, if a buyer offers $500,000 for a property, and the appraisal comes back at $480,000, the buyer might renegotiate the price or withdraw from the contract.

Inspection Contingency

An inspection contingency allows the buyer to have a professional inspection of the property to identify any potential problems. This inspection typically covers structural issues, plumbing, electrical systems, and other aspects of the property’s condition. Based on the inspection report, the buyer can request repairs from the seller, renegotiate the price, or terminate the contract if the discovered problems are significant and unresolvable.

The inspection contingency usually specifies a timeframe for the inspection and a deadline for notifying the seller of any issues. For example, the buyer might have 10 days to conduct the inspection and 5 days to inform the seller of any necessary repairs.

Real Estate Agent and Broker

Navigating the complex world of real estate transactions often requires the expertise of professionals. Understanding the roles of real estate agents and brokers is crucial for a smooth and successful home-buying experience. These individuals act as intermediaries, guiding buyers and sellers through the intricacies of the process, protecting their interests, and ensuring a fair and transparent transaction.Real estate agents and brokers are licensed professionals who facilitate the buying and selling of properties.

While both work in real estate, their roles and responsibilities differ. A real estate agent works under the supervision of a broker, representing either buyers or sellers. A broker, on the other hand, holds a higher level of licensing and can operate their own brokerage or supervise other agents. They are responsible for overseeing the activities of their agents and ensuring compliance with all relevant laws and regulations.

Agent and Broker Responsibilities

Real estate agents are responsible for marketing properties, showing homes to prospective buyers, negotiating offers, and assisting with the closing process. They act as advocates for their clients, negotiating the best possible terms and conditions. Brokers oversee the agents in their brokerage, ensuring they adhere to ethical standards and legal requirements. They are also involved in managing the business aspects of the brokerage, including marketing and financial operations.

A broker may also directly work with clients, particularly in high-value transactions or complex deals.

Importance of Choosing a Qualified and Experienced Agent

Selecting a qualified and experienced real estate agent is paramount to a successful home purchase. An experienced agent possesses a deep understanding of the local market, including pricing trends, neighborhood characteristics, and inventory levels. Their expertise can save buyers time and money, guiding them towards suitable properties and helping them avoid potential pitfalls. A qualified agent will also be knowledgeable about the legal aspects of real estate transactions, ensuring the process is conducted smoothly and legally.

Choosing an agent with a proven track record of successful transactions can significantly increase the chances of a positive outcome.

Effectively Working with a Real Estate Agent

Effective communication is key to a successful working relationship with your real estate agent. Clearly communicate your needs, preferences, and budget to your agent. Regularly check in with your agent to discuss progress and address any concerns. Be prepared to provide necessary documentation promptly and ask clarifying questions if anything is unclear. Trust your agent’s expertise, but don’t hesitate to seek second opinions or additional information if needed.

Remember that your agent is working for you, and a collaborative relationship will result in the best possible outcome.

Home Inspection

A home inspection is a crucial step in the home buying process. It’s an independent assessment of the property’s condition, providing you with valuable information to make an informed decision. Understanding the process and the potential implications can save you significant time, money, and stress down the line.A qualified home inspector will thoroughly examine various aspects of the property, generating a detailed report outlining any issues discovered.

This report empowers you to negotiate repairs with the seller or to walk away from the deal if significant problems are identified. This is your opportunity to identify potential problems before they become costly repairs after you’ve moved in.

The Home Inspection Process

The inspection typically takes several hours, depending on the size and complexity of the home. The inspector will visually examine both the interior and exterior of the property, accessing attics, crawl spaces, and other areas as needed. They use various tools and techniques to assess the condition of different systems and components. The inspector will then compile a detailed report that Artikels their findings, including photographs and recommendations.

This report is typically delivered within a few days of the inspection.

Aspects of a Property Inspected During a Home Inspection

Home inspectors assess a wide range of property components. This includes, but is not limited to, the structural elements of the house (foundation, framing, roof), the plumbing system (pipes, fixtures, water heater), the electrical system (wiring, outlets, panels), the heating and cooling systems (HVAC), and the appliances (oven, refrigerator, dishwasher). They also check for signs of pest infestation, water damage, and other potential problems.

The level of detail can vary depending on the inspector’s expertise and the scope of the inspection.

Implications of Significant Issues During Inspection

Discovering significant issues during the inspection can have several implications. These issues might range from minor cosmetic problems to major structural defects. For example, discovering significant foundation cracks, extensive water damage, or a failing HVAC system could lead to costly repairs. The severity of the problem will dictate your next steps. You might negotiate with the seller to repair the identified issues before closing, request a price reduction to offset the cost of repairs, or even terminate the contract entirely.

For example, if a seller refuses to address a major structural problem identified in the inspection, you might choose to withdraw your offer, avoiding potentially substantial expenses later. Having a strong real estate agent to guide you through these negotiations is highly beneficial.

Ending Remarks

Buying a home is a significant financial undertaking, and understanding the language of real estate is paramount. This guide has equipped you with 15 essential terms to confidently navigate this journey. Remember, while this information provides a solid foundation, seeking professional advice from a real estate agent and financial advisor is crucial. By combining this knowledge with expert guidance, you’ll be well-prepared to make informed decisions, secure favorable terms, and ultimately achieve your homeownership goals.

Don’t let the jargon intimidate you; empower yourself with knowledge and take control of your real estate future.

Common Queries

What’s the difference between a real estate agent and a broker?

A real estate agent works under a broker and is licensed to represent buyers or sellers. A broker is a licensed professional who can operate their own agency and supervise agents.

What happens if my home inspection reveals significant problems?

Depending on the severity and the terms of your contract, you may be able to renegotiate the price, request repairs, or even back out of the deal.

Can I get out of a real estate contract after signing it?

It depends on the contingencies included in your contract and the specific circumstances. Consult with your real estate attorney.

What if I can’t afford my closing costs?

You can explore options like securing a loan to cover closing costs or negotiating with the seller to contribute towards them.

How long is a typical home inspection?

A standard home inspection usually takes 2-3 hours, depending on the size and complexity of the property.